Bootstrapping Guide: How to Start a Business with No Money

Startup advice can be seductive. From motivational quotes to magazine profiles, there’s a persistent narrative that if you follow your passion, log 80 hours a week, and “hustle hard,” you’ll create the next Amazon or Airbnb.

It is possible.

We all know that hard work can produce incredible results. But the prevailing rise-and-grind mythology often pushes founders into business before they’re ready.

Many smart, ambitious people feel pressured to quit their jobs and go all-in. They work around the clock, sacrificing their health and happiness to chase a startup dream.

For every founder who’s battling exhaustion and surviving on protein bars, I’d like to suggest a different path.

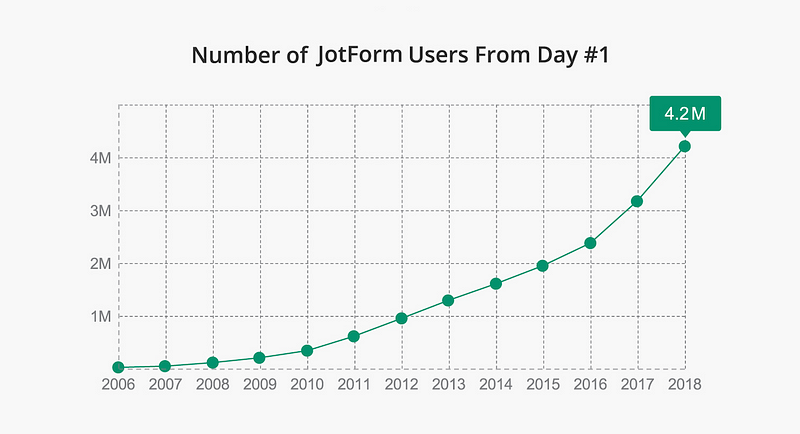

It’s the same path that enabled me to build JotForm in a wildly competitive industry, where even Google is vying for our market share. Since 2006, we’ve grown to serve 4.2 million users and create a team of 130 employees—and we’ve done it without taking a penny in outside funding.

JotForm isn’t an overnight success story, and I certainly don’t have a private jet. But, I’ve built a business I love, while maintaining my freedom and a rich personal life.

Bootstrapping can be a great path for entrepreneurs of every kind. Here’s what we’ve learned—and how it can help you to achieve success on your own terms.

Why small is the new big—the case for bootstrapping

Many founders think venture capital is a prerequisite for success. Reports of record-breaking funding rounds and billion-dollar valuations can certainly make it seem that way.

But investment isn’t the only way to fund a business.

A growing number of founders, or “bootstrappers” are building their companies with little or no outside funding. They don’t have to fuss over investment decks and most could care less about reaching the top of TechCrunch . Very few worry about creating personal brands on Instagram—especially in the early stages. They’re more concerned about serving real customers, who support their ideas with hard-earned cash.

They might not be as visible as entrepreneurs who spend a fortune on PR agencies, but in every industry, you’ll find independent, self-funded companies that are also wildly profitable. For example:

MailChimp co-founder and CEO Ben Chestnut needed to create email newsletters for his design consulting clients. He built a tool to streamline this tedious process, and created a business worth $4.2 billion , with $600 million in annual revenues.

Todoist is a market leader in productivity, used by over 10 million people and organizations including Apple, Starbucks, Google. Amir Salihefendic launched its parent company, Doist, in 2007 and says “we’re running a marathon, not a sprint.”

Basecamp started in 2004, when Jason Fried and his web design firm needed a project management app to keep them organized. They built an internal tool, started using it with clients, and now have nearly 2.2 million customers and employees in 30 cities worldwide.

These are just a few businesses that are racking up customers and profits to rival their VC-backed competitors. One key difference? They get to call the shots about when, where and how they work—and grow. Many of the founders also build their empires quietly, with more concern for creating great products than generating market buzz.

Clearly, bootstrapping isn’t for everyone. Not every business can be self-funded, and sometimes, outside investment is exactly the right choice. We all need to chart our own paths. But bootstrappers remind us to question the prevailing startup narratives and ask, “Do we really need to raise VC money?”

It’s well worth taking a breath, setting the pitch deck aside for a moment, and considering an alternative route.

Self-funding vs raising money: pros and cons

Starting a business isn’t easy. There are risks, challenges, and complications, whether you leverage your own cash or you pursue venture capital. Reading headline after headline about record-setting funding rounds, however, can make VC backing look glamorous—and perhaps even necessary.

Most of us can name the well-funded success stories: Facebook, Google, WhatsApp, Alibaba, Rent the Runway, Uber, and more. But for every famous brand, there are thousands of VC-funded firms that quietly grew and then fizzled. That’s why it’s good to take a clear-eyed look at the statistics.

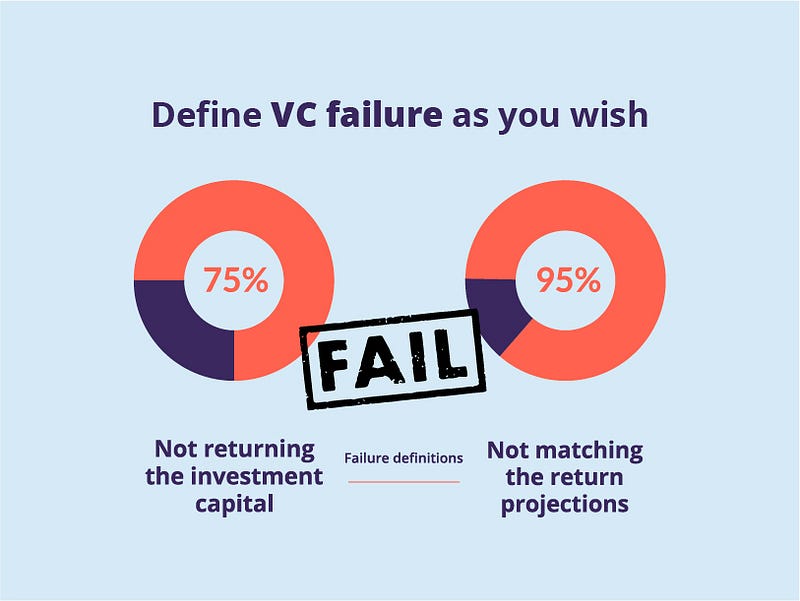

Research by Harvard lecturer Shikhar Ghosh reveals that about 75% of VC-backed companies in the U.S. fail, meaning they don’t return the investors’ capital. If we define failure as not delivering the projected return on investment, however, then more than 95% of startups fail, says Ghosh.

Just like a bicycle, a startup requires some speed to stay upright. But once a founder accepts outside cash, the clock really starts ticking.

Here’s another way to think about it. If VC funding is the fabled hare, then bootstrapping is the tortoise. It’s slow and steady, but it keeps on going (and going and going).

We know that premature scaling is the number one cause of startup failure. Eager new founders often drain their cash on big offices, the latest technology, splashy PR and marketing campaigns, and hiring full teams—long before they’re ready or even need the support. Sometimes their investors push for these outward signs of accomplishment.

Bootstrappers rarely face the same pressures. They don’t have to meet arbitrary timelines or show hockey stick growth charts. Instead, they have the freedom to set their own targets. They make the rules, and, most importantly, they decide what “success” looks like—even if that definition is constantly evolving.

Clearly, bootstrapping doesn’t eliminate all problems. To grow a business without external funding, you have to swim, or you’ll sink fast. You have to be creative and strategic, but that can also make you a better entrepreneur. Here are three more advantages of taking the self-funded route.

You learn by wearing all the hats

It doesn’t matter if you’re a designer, product engineer, developer, or a UX specialist. As a bootstrapped founder, you’re probably also shipping packages, answering calls, and writing social media posts. That’s how it goes. And while spending precious time on the “other stuff” can be frustrating, it ensures you understand every corner of the business. Once it’s time to hire someone for that role, you know exactly what to look for and what to avoid.

*Quick tip: At JotForm, we hire and grow slowly. And we hire someone only when we have their entire first-year salary in the bank. It’s a simple rule of thumb that has helped to keep us on track.

Needs override wants

The classic (or clichéd) startup office is a former industrial space with exposed beams and high ceilings. It’s bright and it shows the company is Doing. Big. Things. Until a business truly needs that kind of space, however, it’s not a smart expense.

It’s easy to get distracted, but bootstrappers can make strategic choices, like using open-source software and upgrading later, if necessary. Or working from home, renting a desk in a co-working space, and doing the PR and accounting until you can afford to get help.

Remaining lean allows you to pivot

In the early stages of a startup, the business is still pliable. You can release a product, gather user feedback, and adapt to real market needs. That’s an advantage.

Entrepreneurs often chase perfection, but it’s not only impossible; it can put your company at risk.

New founders should release their products as soon as possible. Don’t even try to make it perfect. Hundreds of startups have adapted and pivoted their way to success:

- Instagram started as a check-in app called Burbn, until founders Kevin Systrom and Mike Krieger offered viral photo filters with a streamlined interface.

- Slack was originally developed to support a now-defunct game called Glitch. Founder Stewart Butterfield soon realized that the internal messaging app, not the game, was the real opportunity.

- YouTube was a dating site until founders Jawed Karim, Steve Chen, and Chad Hurley dropped the “singles” videos and opened the platform for all kinds of uploads.

When startups work obsessively to create the “ultimate” first release, they can also be tempted to argue with their customers—even when customers share honest feedback about what they want and need. That’s why staying lean and flexible can be a major business advantage.

How to get started with bootstrapping

5 Essential Stages You Have To Consider Before You Bootstrap a Business

- Keep your day job

- Start a side project

- Share what you create

- Always pursue problems, not passion

- Stay close to your product

After college, I spent five years working as a programmer for a New York-based media company. I learned so much there: how my mentors accomplished their goals and how to collaborate with team members. I also saw how micromanagement destroys staff motivation. Most importantly, that’s where I got the idea for JotForm.

Both startup press and social media often advise founders to leap blindly into business as soon as they have an idea. That approach can work, but it’s a tough slog that kills lots of promising companies. Instead, there are five steps you can take—right now—to lay the foundation for lasting success.

1. Keep your day job

Writing a manifesto and leaving your job with a flourish, Jerry Maguire-style, might seem like a badass entrepreneurial move. Unfortunately, it didn’t even work for Jerry.

Most bootstrappers test the waters with a side project while they hold down a full-time gig. They leave the safety of a regular paycheck only when that side hustle can provide viable, long-term income. SpaceX, Apple, Product Hunt, Trello, WeWork, Craigslist and Twitter all started this way.

Never underestimate how much you can learn and accomplish in a 9-to-5 job—and let’s all agree to stop saying “day job” like it’s a four-letter word. Getting paid to sharpen your skills at a healthy, productive company can provide a great foundation for whatever you’re building.

2. Start a side project

At Google, employees can spend 20% of their time exploring new ideas or creative projects. This 20% time policy is well known in tech circles, but it’s a concept we can all apply to our work lives.

We can build entire businesses by tinkering on the side, but most importantly, side projects boost creativity. When there’s no pressure to meet a revenue target (or make any money at all), we’re free to play, explore and learn. It’s a great way to decide whether the project truly captures your imagination, and to gauge outside interest.

In fact, side projects should be stupid, says ex-Spotify product designer Tobias van Schneider:

“The only way a side project will work is if people give themselves permission to think simple, to change their minds, to fail—basically, to not take them too seriously.

When you treat something like it’s stupid, you have fun with it, you don’t put too much structure around it. You can enjoy different types of success.”

We should never be afraid to invest time and energy into something that excites us; something that gets the blood pumping and our creativity flowing. Follow curiosity and see where it leads.

And if enabling “stupidity” doesn’t work, trying looking at the side project through a more scientific lens.

Don’t focus on the outcome or how the experiment will be received. Just start.

3. Share what you create

Even before it’s done, and long before it’s “ready,” we need to share our ideas. Show people what you’ve been working on—this was one of the strategies that helped us to land our first 1,000 users. Take them inside the experiments you’re running, no matter how early or unpolished.

Today, there are so many different and inexpensive ways to share. Pick your favorite platform—the one that feels natural, and where you spend time anyway. It could be a YouTube channel, an Instagram account, a podcast, or even a blog. I have my blog on Medium but it could be whatever other network that works for you.

The simple act of sharing can help you to:

- Develop an engaged audience (even if it’s small) before you launch a startup or try to sell what you’re creating.

- Refine your ideas. Explaining a concept to someone else is the quickest way to find invisible holes. Use that pre-launch time to get smarter and fill your own knowledge gaps.

- Develop a solid track record. Business is more than a financial transaction; it’s built on trust. When you show the work and bring people along for the ride, they get to know you. They feel invested. They see that you’ve consistently shown up, provided valuable content, and followed through on what you started.

Keep learning. Stay hungry.

As we collect that paycheck and play with new ideas, it’s the perfect time to learn. Never before have there been so many expert voices and resources, right at our fingertips. We can take online courses, read blogs, watch videos, attend meetups, listen to interviews, and read books. Find mentors (both real and virtual) and soak up every bit of knowledge possible. Then, apply what you lean and keep experimenting.

4. Always pursue problems, not passion

Contrary to prevailing wisdom (and motivational quotes), the best startups aren’t driven by passion; they solve problems. We built JotForm to eliminate a friction point that I experienced firsthand, while working at the media company.

Back in the late ’90s, building custom web forms was tedious and time-consuming, so I envisioned a drag-and-drop tool that anyone could use. I knew people wanted the product, because it solved a problem we struggled with every day.

Investor and Y Combinator co-founder Paul Graham says the most successful business ideas share three common features: They’re something the founders themselves want, that they themselves can build, and that few others realize are worth doing.

“The verb you want to be using with respect to startup ideas is not ‘think up’ but ‘notice,’” writes Graham. “At YC we call ideas that grow naturally out of the founders’ own experiences ‘organic’ startup ideas. The most successful startups almost all begin this way.”

Ask yourself:

What problems have you experienced in the world?

What problems do you have with products, services, and even yourself?

Problems need smart solutions. Passion is just the icing on the cake.

Who needs this now?

The RXBar also came from a personal need. Company CEO and co-founder Peter Rahal wanted a deliciously simple protein bar free of chemicals or synthetic ingredients. So, he developed a nutritious bar that would satisfy the CrossFit-going, paleo-eating crowd—and himself.

Rahal and his business partner, Jared Smith, scratched their own itch. As Basecamp founders Jason Fried and David Heinemeier Hansson write in their bestselling book, Rework, “the easiest, most straightforward way to create a great product or service is to make something you want to use.”

Once you have a prototype, it’s time to ensure you have an eager customer today , not sometime in the future.

If you can’t answer the question, “who needs this right now?” it might not be a viable business. For example, Rahal kept re-mixing his recipes until they tasted incredible. He didn’t stop until he knew people would pay for the product—and he tested that threshold by selling the bars, door to door, packaged only in Tupperware.

5. Stay close to your product

Using what you create can be a game-changer. And it sounds so simple; after all, who wouldn’t use the product they built? But a startup has so many moving parts that founders can quickly become detached from their original mission.

Once a product or service is shipping, it’s important to stay close to the heart of your offering. Use it, consume it, order it, and dig into the details. Engagement puts you back in the customer’s shoes, so you experience any problems firsthand. It also keeps the team (no matter how small) on its toes.

Additionally, If the startup was built to scratch your own itch, there are always more opportunities to extend the solution. Ask yourself:

How else could this product serve me, personally?

What would make this solution more valuable—both to current and potential customers?

Very few problems in life are tackled once and solved forever. Startups aren’t stagnant, either. They need to evolve with needs, culture and markets. When you keep mining the problem (and the solution), it can keep the business fresh and vibrant.

Should you commit to a co-founder?

Sonny and Cher. Bert and Ernie. Calvin and Hobbes. Thelma and Louise.

Pop culture loves a good duo. So does the startup world.

Investors like Paul Graham often want to back businesses run by partners with complementary skills. Apple, for example, paired the late, sales-savvy Steve Jobs with Steve Wozniak, who focused on technology.

But when co-founders don’t gel, the results can be disastrous. “Startups do to the relationship between the founders what a dog does to a sock,” says Graham. “If it can be pulled apart, it will be.”

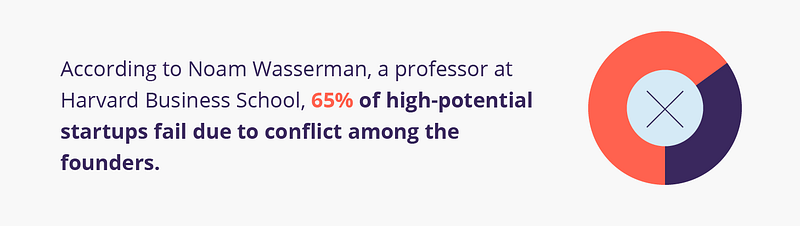

According to Noam Wasserman, a professor at Harvard Business School, 65% of high-potential startups fail due to conflict among the founders. Wasserman studied 10,000 entrepreneurs for his book, The Founder’s Dilemma, and suggests that multiple founders bring more skills to the table, but they also have more potential for disputes over money, strategy, leadership, credit, and other issues.

It makes sense. Multiple founders can get behind the wheel, but they have to agree on the destination, plus everything from who’s in the back seat to the best driving route. Many founders also have a strong desire for freedom, which can quickly feel stifled when someone else weighs in on every detail.

Sign on all the dotted lines

“Picking a co-founder is your most important decision,” says Naval Ravikan, co-founder of the AngelList platform. “It’s more important than the product, market, and investors.”

Ravikan makes a bold statement. Not everyone would agree that the partnership matters more than the product—or the market. But starting a business is a massive commitment. You’re picking someone with whom to share your life’s work. You’ll also share money, space, risk, and a whole lot of time.

The right partnership is powerful. Working with the wrong person can feel heavy and frustrating (at the very least) and, in the worst case, it can destroy the business.

That’s why a founders’ agreement should be excruciatingly detailed. Hire an experienced lawyer, if you go this route, and plan for everything: equity breakdown, vesting schedules, intellectual property, termination clauses, and more. Ensure that everyone is clear on the terms and feels fully protected, should the partnership go south.

You can go it alone

If you’re not sure about a potential co-founder, there’s no reason to rush. As I explained in Why you don’t need a co-founder to start your own business , take your time and see how it feels to work on your own.

Forget what the VCs say—especially if you’re prepared to bootstrap. As Ravikan says, “if you’re compromising, keep looking. A company’s DNA is set by the founders, and its culture is an extension of the founders’ personalities.”

Entrepreneurs who do trust themselves to go solo are often rewarded with the ultimate freedom. Spanx founder Sara Blakely, for example, built a global company without a co-founder or any outside investment. At age 41, she became the youngest self-made female billionaire—and she still owns 100% of the company.

Entrepreneurs, of all people, should know that rules are meant to be broken. That’s half the fun. So, partner up or stay solo, but do it on your terms, with your eyes wide open.

Slow growth is the new hockey stick curve

4 Reasons to Grow Your Business Slowly

- Focusing on profits creates freedom

- You can build the right team, not a “right now” team

- Moving slowly can make customers happy

- There’s time and space for learning

Most startup experts worship at the altar of rapid expansion. They even have a pattern for it, called “hockey stick growth,” which occurs when revenues start out flat and then quickly shoot up to create that iconic curve.

“Aiming for hockey-stick growth, while being aware of the predictable stages of growth, is exactly what successful entrepreneurs should do,” writes entrepreneur Bobby Martin, author of The Hockey Stick Principles .

Investors dream about rapid growth, too. They want to recover their money fast, so they often pressure companies to expand quickly.

A hockey stick looks great on paper, but it typically requires the business to grow revenues first and figure out profits later. That can put the company at risk. Bootstrappers take the opposite approach. They sort out profits first and stay focused on that key goal.

Slow growth takes patience and a good dose of bravery. It’s normal to feel some FOMO as you watch other firms double, then triple their staff overnight. But slow growth can provide stability. It also enables founders to sleep well at night, spend time with the people they love, and create products that attract loyal, satisfied customers.

Here are four more reasons to take the slow road.

1. Focusing on profits creates freedom

Bootstrapping math is pretty simple: spend less than you earn and you can grow at your own pace. It’s simple, but it’s not effortless.

When we celebrate companies that raise millions and post huge vanity metrics, like user acquisitions, that math can seem almost too simple.

Glorifying hockey stick growth also implies that you can chase flashy numbers now and worry about profits later. In today’s market, it’s not uncommon to hear the question, “how, exactly, do they make money?”

But profits provide freedom—even when they’re modest. Make decisions that keep your company in the black, right from day one. After all, a bootstrapped business needs to work, because there are no hefty bank deposits to fall back on.

2. You can build the right team, not a “right now” team

Newly-funded companies often face pressure to fill every seat—immediately. “Hire fast, fire faster” has even become a startup mantra. There’s a sense that Christmas is coming, so Santa better hire as many elves as possible. It doesn’t matter if they’re out of work by February.

Building the right team is essential. These are the people who will build and nurture the product. They’ll implement new ideas and interact with customers. As Todoist founder Amir Salihefendic says, “Optimize on output. Don’t optimize on the number of people you hire.”

3. Moving slowly can make customers happy

Caring about customers is good for business. That’s not a tagline; it’s an effective way to bootstrap. VC-backed companies often start out with deep knowledge of their audience. Over time, though, it’s easy to confuse what customers want with what investors want.

If you believe that growth reigns supreme, then it will quickly become the primary focus.

“Traction and product development are of equal importance and should each get about half of your attention,” says Gabriel Weinberg, a successful CEO and the author of Traction. “This is what we call the 50 percent rule: spend 50 percent of your time on product and 50 percent on traction.”

4. There’s time and space for learning

Very few people are born knowing exactly how to lead—or to design, code, market, sell, and build. Aggressive growth can quickly highlight those knowledge gaps, which are totally okay. Most people launch businesses to create a smart solution, not because they want to run staff meetings.

Growingly slowly enables you to learn alongside your team. You can learn how to manage and motivate those people, too. Mistakes can also be smaller when you’re not feeling the heat from investors, or you suddenly see 50 new faces in the office, all eager for direction. Take your time and you can:

- Create effective onboarding processes that set new employees up for success

- Get to know people on a human level, not just as “employee #43”

- Ensure new team members absorb important values, like openness, honesty, and a willingness to take risks

The power of customer-centric growth

Customers. As we focus on funding options, it’s easy to leave end users out of the conversation. Even the term “users” dehumanizes the people who will buy what we create. But bootstrapped companies ultimately answer to their customers, not to investors. We have an obligation to listen closely to customer needs , feedback , and ideas—and that’s a good thing.

Even criticism is great for business, because it pushes the team to stretch and innovate. Customer-funded growth keep us honest; they ensure we don’t stray off track. That’s a powerful advantage.

Test and change. Then test again.

Never assume you know what customers want; you have to look at the data. We’re lucky to live in an era where we can create a hypothesis and then test it without overt bias. Making a product change? Release it to a small group and establish a clear way to measure user reactions. Apply what you learn and test again.

Testing doesn’t mean you’re beholden to customer whims, either. You create the “what,” and customers help to show you “how.” For example, Airbnb’s mission is to create “a world where people can belong through healthy travel that is local, authentic, diverse, inclusive and sustainable.” How, exactly they do that is still up to the smart people running the company.

Get serious about customer support

According to surveys conducted for American Express:

- More than half of Americans have scrapped a planned purchase or transaction because of bad service

- 33% of Americans say they’ll consider switching companies after just a single instance of poor service

- U.S. companies lose more than $62 billion annually due to poor customer service

- As a group, Millennials are willing to spend the most (an extra 21%) for great customer care

The numbers are clear: customer service matters deeply. Support teams do much more than resolve tickets and answer tedious questions; they have a massive effect on company growth.

Sexy customer acquisition stats usually get the spotlight, but it’s better to spend time, energy, and money on satisfying existing customers than winning over new ones. In fact, data shows that it’s anywhere from 5 to 25 times more expensive to acquire a new customer than to keep a current one.

Extraordinary customer support doesn’t even require extraordinary efforts; you just need to consistently exceed expectations:

- Hire support staff as methodically as you hire for other roles. Talk to top support team members (even if that’s one person, for now) and create a formula. Identify key traits, must-have skills, and nice-to-have qualities. Use what you learn as a litmus test for hiring.

- Put customer support at the center of product innovation. Encourage support teams to speak up and contribute to the innovation pipeline. Empower them to investigate the issues they encounter, instead of operating as script-reading robots.

- Enable them to take initiative. Don’t make support team members ask permission to bend the rules, issue a refund, or send a replacement item. And give them the power and resources they need to delight customers.

- Develop a reliable knowledge centre. In-depth FAQs allow customers to find simple answers fast, which reduces strain on support teams. Also, create loops that ensure the feedback that arrives through this channel is actionable.

- Review processes on a regular basis. Update systems and processes as needed, especially during times of growth. Create rituals for staff to share updates, discuss issues, explore positive feedback, and simply check in.

- Say thank you. Reward your support teams on a regular basis. Treat them well. These people are life-savers, and they deserve our gratitude.

Don’t let a startup compromise your sanity

Bootstrapping is not a great way to get PR. And most self-funded entrepreneurs are too busy refining their product to worry about landing on magazine covers.

A little publicity certainly never hurts but what does the attention really do—especially if it’s about the business, not the product itself? Most customers don’t read industry or tech publications anyway. Once the attention fades, you’re still left with the same mission and the same challenges.

Highly-publicized funding rounds can also put you under a microscope. For example, Nasty Gal founder Sophia Amoruso made headlines in 2016 when her fashion brand filed for Chapter 11 bankruptcy protection, after raising $65 million over 10 years.

Now that she’s launched a new venture, called Girlboss, both critics and fans are tracking her every move. Many other founders have been in Amoruso’s shoes, too. Well-funded startups that crash and burn often make headlines. With serious money often comes serious scrutiny.

Big-time investments can supercharge the startup (for better or worse), but slow growth can ensure you have a sane, happy personal life—even as you build a thriving business. Here’s why.

More downtime = better results

Most people think success requires 16-hour days. Typically, the opposite is true. Busy and effective are not the same thing—even though “busyness” has become a modern-day status symbol.

“Hustle might move you forward, but it doesn’t set you up for sustainable success,” says Kyle Young, author of QuitterProof. “Good habits are formed through consistency and repetition, not mindless effort.”

Many of the world’s greatest innovators (past and present) dedicated large amounts of time to simply thinking. Reflecting. Strategizing and planning. Bill Gates originally made the Think Week famous. Now, other founders, like Skillshare’s Mike Karnjanaprakorn, have adopted this practice. Steve Jobs, Mark Zuckerberg and Tim Ferrriss have also followed suit.

Taking a digital sabbath can also keep you feeling rested and ready to play the long game. On Saturday, Sunday or another day of your choice, avoid technology in all forms. For example, power down your laptop and place it safely out of sight. Shut off your smartphone and hide it in a drawer. Change your Netflix password—and then try to forget it. Give your brain the gift of peace, and the time to reflect and generate new ideas.

Remember that “overnight success” is a myth

51: That’s how many games Mikael and Niklas Hed created before they launched Angry Birds , which saved their company, Rovio, from bankruptcy.

25: That’s how many publishers rejected Tim Ferriss’ The Four-Hour Workweek before Harmony Books offered him a contract. The 2007 title has now sold over 1.3 million copies to date.

9: That’s how many months Anna Wintour spent at Harper’s Bazaar before she was fired, apparently for producing photo shoots that were “too edgy.” Wintour went on to become one of the most powerful women in fashion, serving as Vogue magazine’s editor-in-chief for over 40 years.

Founders are often hungry for success, but it takes time. Often, lots of time. A sustainable business model gives you the freedom to enjoy the ride. You can focus on building something you love, and that truly serves your customers, instead of racing toward empty growth targets.

How to play (and love) the long game

“So, what’s your exit strategy?”

Entrepreneurs often hear this question before they’ve earned a single dollar?—?and it can be disorienting. When you’re still building a business you love, why would you think about selling it?

Just as there are marked differences between bootstrapped and VC-backed founders, “exit strategies” often divide entrepreneurs into two camps: those building to sell, and those who are in it for the long run.

Either scenario has merit. Business is personal, and we all need to make our own choices. Although some bootstrappers will eventually sell their firms, they rarely begin with this goal in mind.

“What’s better than an exit strategy?” says Todoist founder Amir Salihefendic. “It’s a long-term mission that your company truly cares about. It’s focusing on building a company that can outlast you and creating something of true value.”

Create value first and valuation will follow. Bootstrapping forces you to develop a product that’s worth paying for instead of trying to reach the top of TechCrunch or building a house of cards on a shaky foundation.

As I mentioned in Building my startup for 12 years: how to win the long game , you can retain your values, freedom and flexibility. You can learn from a slow-burning journey. You can focus on the long-term rather than the short.

Sustainable growth = survival

A study from the National Bureau of Economic Research found that unicorns (private companies valued above $1 billion) are roughly 50% overvalued. They’re not generating billions of dollars in revenue, but thanks to deep-pocketed investments, paper valuations swell to reach that 10-figure sum.

Relying purely on estimates can be risky, because a sky-high valuation demands rapid scaling. And if the sky suddenly falls, VC-backed startups are often left in a vulnerable position. As Warren Buffet once said, “It’s only when the tide goes out that you can see who’s been swimming naked.”

The media may glorify fast movers and big wins, but playing the long game is another type of victory. In fact, slow growth doesn’t have to be a mere consequence of bootstrapping; it can be a smart, deliberate choice.

If you measure success against lofty goals, it’s easy to feel discouraged along the way and devastated if you don’t reach them at all. Instead, each new milestone can be something to celebrate.

“There is power in small wins and slow gains,” says James Clear. “This is why average speed yields above average results. This is why the system is greater than the goal.”

It’s worth exploring asking yourself:

- Where am I trying to go?

- What do I gain by getting there quickly?

- What am I prepared to sacrifice by making speed part of my strategy?

For many bootstrappers, a harmonious work culture, plus total creative and financial freedom is the ultimate compensation.

Nurturing a healthy culture

In the hard-driving startup world, “culture” can be a cliché topic. Tech companies became infamous for installing foosball tables and offering craft beer on tap in exchange for gruelling work schedules. Superficial perks don’t foster culture—or a healthy work-life balance.

At JotForm, we aim to work in a way that’s sane, friendly and open. We keep normal hours and try to treat each other with deep respect. We also believe actions speak louder than words.

Enron Corporation—the American energy, commodities and services company—had four stated values: respect, integrity, communication and excellence. But those “official” values didn’t save the company from a high-profile bankruptcy and auditing scandal that sent several top executives to prison.

Culture grows through big choices, like team structure, transparency, and product-focused goals. It also emerges through smaller actions, like when the founder preaches balance and leaves the office by 6 pm every night.

As you begin to grow and hire a team, here are five ways to encourage a rich, healthy startup culture:

- Give employees the tools they need to thrive. From big monitors to space for sketching and computer work, it rarely makes sense to skimp on the resources that allow people to do their best work.

- Study the qualities of standout employees. From personal traits to education and skills, what kind of people move the organization forward? Try to capture both the intangible and concrete qualities you hope to foster, and then use them to inform recruiting, hiring, and promotion.

- Set the tone you seek. “If you are lucky enough to be someone’s employer,” says Whole Foods CEO John Mackey, “then you have a moral obligation to make sure people do look forward to coming to work in the morning.” Culture is a major asset that helps organizations to attract top-notch people and encourage them to stay .

- Don’t enable incongruent behavior. All JotForm interns, regardless of their position, spend their first week answering customer support questions. We rate their skills and how they treat our customers. Do they listen? Are they patient and encouraging? If someone thinks support work is beneath them, that attitude is incongruent with our company. It doesn’t matter how skilled or talented they might be; they won’t receive a job offer from us.

- Remember that culture is constantly changing. Which comes first: great people who establish a healthy culture, or a healthy culture that attracts great people? It doesn’t matter. Startup culture has its own equilibrium, and small changes can have big effects. Keep tabs on how employees are feeling. Watch how they treat each other—and your customers. Encourage healthy behavior and choose positive, collaborative people.

A few final words

Bootstrapping is just one way to build a business. Capital-intensive industries such as energy, transportation, telecommunications, and brick-and-mortar stores and restaurants often require funding. VC backing might also be the best way to achieve your business goals and personal ambitions.

For anyone who’s eager to control their entrepreneurial destiny, bootstrapping can be an excellent choice. It worked for me, and I hope it can work for you, too.

Yes, it takes patience, drive, and determination. But the payoffs can include freedom (both financial and personal) and a better sense of work-life balance. You can grow at a sane pace and maintain a healthy personal life.

A self-funded business can also achieve great financial success. It might take more time, but the journey is often far more enjoyable. You can develop a product that improves people’s lives and build a top-notch team to help you along the way. You don’t have to feel like an imposter, either, because there’s time to learn and evolve with your business, not in spite of it.

Slow, sustainable growth is possible.

Stay focused on your product, trust in your abilities, and ask for help when you need it.

You can do this.

Originally published at https://www.jotform.com on July 8, 2019.

This is really interesting article. I have been hearing lot of people talking about capital before starting business. This is the best answer to their questions.

Wow what an inspirational and useful guide to the young entrepreneurs, Thank you.

Thank you for this information

thanks for this amazing blog

Thanks, your articles are always worth reading.

thanks for sharing information about Start a Business with No Money, nice post

i appreciate yor article

keep sharing and good luck